Publications > Editions EMS > Les corridors de transport > Corridors of the Sea: An investigation into liner shipping connectivity

|

Par

Jan Hoffmann

Par

Jan Hoffmann

Chief, Trade Facilitation Section, TLB, DTL

United Nations Conference on Trade and Development

(UNCTAD) Geneva - Switzerland

Biographies

Jan

Hoffmann works as trade facilitation, port

and shipping specialist at UNCTAD Trade Logistics

Branch since 2003, currently as Chief of the organization

Trade Facilitation Section within the Trade Logistics

Branch. He is, inter alia, in charge of various

trade facilitation projects on multilateral and

regional trade facilitation negotiations, as well

as regional and national projects Africa, Asia and

Latin America. He edits the quarterly UNCTAD "Transport

Newsletter" and the "IAME-News", and he is co-author

and coordinator of the annual UNCTAD "Review of

Maritime Transport".

Jan

Hoffmann works as trade facilitation, port

and shipping specialist at UNCTAD Trade Logistics

Branch since 2003, currently as Chief of the organization

Trade Facilitation Section within the Trade Logistics

Branch. He is, inter alia, in charge of various

trade facilitation projects on multilateral and

regional trade facilitation negotiations, as well

as regional and national projects Africa, Asia and

Latin America. He edits the quarterly UNCTAD "Transport

Newsletter" and the "IAME-News", and he is co-author

and coordinator of the annual UNCTAD "Review of

Maritime Transport".

Previously, he spent six years with the United Nations Economic Commission for Latin America and the Caribbean (ECLAC) in Santiago de Chile, and two years with the International Maritime Organization (IMO) in London and Santiago. Prior to this, he held part time positions as assistant professor, import-export agent, translator, consultant and seafarer for a tramp shipping company.

Jan has studied in Germany, United Kingdom and Spain, and holds a doctorate degree in Economics from the University of Hamburg. His work has resulted in numerous UN and peer reviewed publications, lectures and technical missions, as well as the Internet "Maritime Profile, the "International Transport Data Base, the "Liner Shipping Connectivity Index, and various electronic newsletters.

Introduction: Transport networks and connectivity

Liner

shipping services form a global maritime transport

network which moves most of the international trade

in manufactured goods. Although the share of air-borne

trade has been growing over the last decades, maritime

transport continues to be the dominant mode for

long-distance transport. Excluding intra-EU trade,

it is estimated to account for 90 per cent of the

volume and 80 per cent of the value of international

trade.4

The exact share varies in different estimates, depending

e.g. on whether you include or not trade within

Customs Unions, whether you look at door-to-door

transport or just the leg until the border, or whether

you count tons or ton-miles.5

Whatever method of estimation is used, sea-borne

trade is in any case the by far dominant mode of

transport for international trade.

Liner

shipping services form a global maritime transport

network which moves most of the international trade

in manufactured goods. Although the share of air-borne

trade has been growing over the last decades, maritime

transport continues to be the dominant mode for

long-distance transport. Excluding intra-EU trade,

it is estimated to account for 90 per cent of the

volume and 80 per cent of the value of international

trade.4

The exact share varies in different estimates, depending

e.g. on whether you include or not trade within

Customs Unions, whether you look at door-to-door

transport or just the leg until the border, or whether

you count tons or ton-miles.5

Whatever method of estimation is used, sea-borne

trade is in any case the by far dominant mode of

transport for international trade.

Within maritime trade, there are two major types of service, called "liner" and "tramp" shipping. Liner shipping mostly caters for containerized trade in manufactured goods and certain agricultural products such as coffee, as well as most refrigerated cargo, while tramp shipping is the dominant type of service for bulk cargo, such as iron ore, coal or oil. In tramp shipping, there are no regular services, but a trader would usually charter a whole ship to have his cargo moved from A to B. In liner shipping, on the other hand, a carrier deploys a number of ships on a fixed route, usually covering several ports, and transporting cargoes for a large number of traders.

In non-technical terms, the difference between "tramp" and "liner" can be illustrated by comparing different types of bus services. If your kids go on a school trip, the school may charter an entire bus for this specific trip; there will only be children from this school on this trip, and the time, place and price are negotiated with the charter bus company, just as in "tramp" shipping. If, however, your kids take a public bus to go to school in the morning, there will be a bus "line", with fixed departure times (which you can’t negotiate) and with many other passengers on the same bus. This is comparable to the liner shipping service, where your container will be on the same ship as other containers belonging to many different owners. When we talk about liner shipping connectivity, we look at a network of regular container shipping services. Thanks to containerization and the global liner shipping network, small and large importers and exporters of finished and intermediate containerizable goods from far away countries can trade with each-other, even if their individual trade transaction would not economically justify chartering a ship to transport a few containers from A to B. Thanks to regular container shipping services and transhipment operations in so-called hub ports, basically all coastal countries are today connected to each other. To illustrate the point, think of the Paris Metro, which is also a network of "lines", and you can calculate how many "transhipments" you may need to get from "Gare Montparnasse" to "Rue de la Pompe". Your property will probably be of higher value if it is close to a well-connected tube station (e.g. Châtelet) rather than one with just one line (e.g. Bel Air).

By the same token, the level of "connectivity" to the global liner shipping network varies. There is probably consensus that traders in Singapore are better connected to over-seas markets than traders in Tonga, and most colleagues would likely agree that the connectivity of Morocco today is higher than 10 years ago, thanks to more and bigger ships providing new services to the enlarged port of Tanger. What we are trying at UNCTAD is to capture these different levels of connectivity and trends over time through our annual "Liner Shipping Connectivity Index" (LSCI), published since 2004.6

UNCTAD’s Liner Shipping Connectivity Index

The Liner Shipping Connectivity Index (LSCI) is generated from five components, each one of which is considered to be a possible indicator of a country’s "connectivity":

- 1The number of companies that provide services from/to a country’s ports. Note: These companies do not need to be operated or owned by nationals of the same country. In fact, in the large majority of cases, a country’s trade is mostly moved by foreign companies, and all major carriers earn most of their income transporting third countries’ imports and exports. The more carriers compete for my country’s trade, the more choices I have and the lower are likely to be my freight rates.

- The size of the largest ship that is deployed to provide services from/to a country’s port, measured in Twenty foot Equivalent Units (TEU). This is an indicator of economies of scale and infrastructure. Ports need to provide adequate equipment, such as ship-to-shore gantry cranes, and dredge their access channels to allow for large containerships to be deployed.

- The number of services that connect my country’s ports to other countries. Taking again the example of the Paris Metro, the more lines pass through my station, the more likely I am able to get to my final destination directly, without the need for transhipments.

- The total number of ships that are deployed on services from/to my countries’ ports. While on its own, this information does not necessarily mean that I have a high frequency of services, ceteris paribus, a larger number of vessels is likely to imply a better connectivity.

- The total container carrying capacity of the ships that provide services from/to my countries’ ports, measured in TEU. While on its own, this information does not necessarily mean that my country’s importers and exporters can actually make use of this capacity (the ships may in theory be full), a larger total TEU capacity is likely to imply more available space.

The data for these five components is obtained annually, in the month of July, through Containerisation International on-line.7 CI-Online obtains its data directly from the liner shipping companies, who have an interest in informing shippers (i.e. importers and exporters) of their services. While on occasions we have had evidence that the data is not always fully updated, as carriers fail to inform in time about revised services patterns, overall we have found that the data reflects the true situation of the deployment of the world’s containership fleet. Above all, the information we thus use to generate the LSCI is based on hard data, and not on perceptions (as is largely the case for the World Bank’s Logistics Performance Index LPI)8 or polls among a sample of experts (as is largely the case for the World Bank Doing Business rankings).9 In fact, the underlying data of the LSCI is not just a "sample", but covers the reported deployment of each and every containership at a given point in time (July of each year). This methodology also allows for comparisons over time, as the "sample" is always complete and not dependent on whom we ask.

Obviously, there could be many alternative and more comprehensive ways of creating an "index" to measure liner shipping connectivity.10 In particular, more detailed information on actual frequencies of services could be added, or we could incorporate information on the connections themselves, i.e. with how many other countries am I connected through direct services etc. While we have obtained such type of information for some regions or some years, in the end we had to make a choice between resources (work time) to be deployed against the improvements this would make to the index. Whenever we added more comprehensive measures, the final result in terms of countries’ rankings or trends over time did not really change. Today, the LSCI is increasingly being incorporated in research on trade competitiveness, and it is included in other, broader data bases and indexes, such as World Bank Development Indicators11, Tradingeconomics,12 and the World Economic Forum.13

Trends in the LSCI and its components

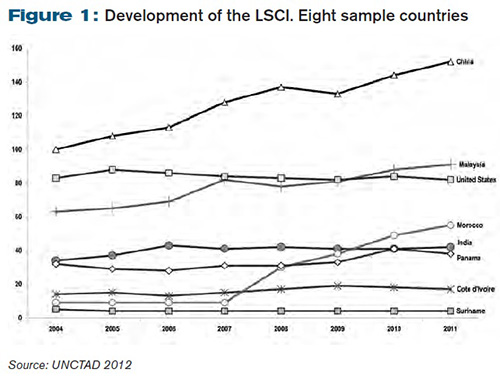

Figure 1 depicts the development of the LSCI of eight selected countries. China continues to lead, and the economic crisis led to a short downturn in 2008; Malaysia has overtaken the United States; and Morocco has surpassed a number of other countries. In July 2011, China continued to lead the LSCI ranking, followed by China (Hong Kong), Singapore and Germany. 111 countries increased their LSCI in between 2010 and 2011, five countries saw no change, and 46 recorded a decrease.

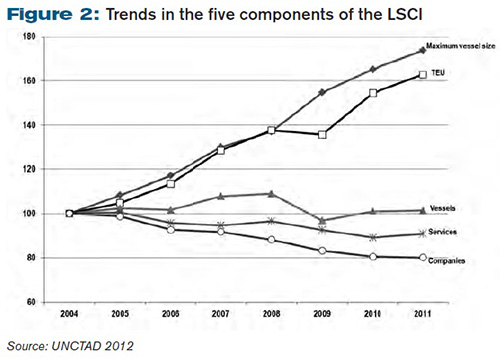

Figure

2 depicts the development of the 5 components of

the LSCI. On average (i.e. the statistical mean

of the 162 countries covered by the LSCI), the size

of the largest vessel has increased by 74 per cent

between 2004 and 2011. Even though the largest new

ships built since 2008 were not bigger than those

built in 2007 (i.e. the Emma Maersk type), on average

the ships that have entered service since then have

more TEU than the existing fleet.

The chart also illustrates the impact of the economic

crisis of 2009, when many ships were idle and thus

not deployed / included in our LSCI. Another trend

that can be observed by analysing the LSCI component

is the continued process of concentration. Although

there have not been many mergers and acquisitions

among carries in recent years, the average number

of services providers (with their own deployed ships)

per country has decreased by 20 per cent between

2004 and 2011.

Unfortunately, we only started the systematic gathering of data in 2004 and do not have comprehensive earlier statistics. Based on anecdotal evidence from several Latin American countries, I believe that about 10 years ago we reached a peak in the average number of companies per country.14 Until the end of the 1990s, many of the large liner companies were still expanding into new markets. Evergreen, MSC and many others did not have services from/to many Latin American and Caribbean destinations. As they expanded, in line with growing containerized trade, the average number of companies per country was effectively still growing. Today, as the major carriers are now covering practically all regions, any consolidation among them leads to a reduction of the average number of companies per country.

Both trends - the larger ships and the smaller number of carriers per country - are two sides of the same coin. On the one hand, larger ships allow achieving economies of scale, which (in a functioning free market) would translate into lower freight costs to shippers. On the other hand, the larger ships require larger companies, which often means that smaller players are squeezed out of the market, which in turn may lead to less competition. If the reduced competition leads to an oligopolistic market structure, it is no longer assured that the reduced costs will effectively be passed on the client.

Liner shipping connectivity and trade competitiveness

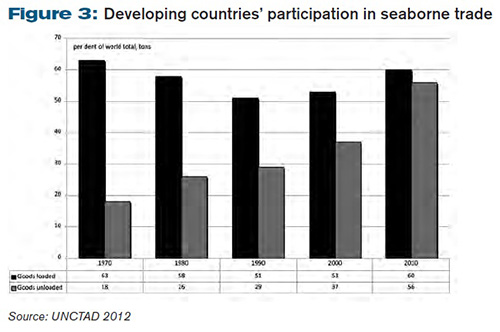

Why would UNCTAD care about its member countries’ shipping connectivity? When UNCTAD first produced its annual Review of Maritime Transport more than 40 years ago, it was mostly concerned about developing countries’ participation in the control of national "fleets", i.e. the ownership and registration of bulk and general cargo ships. Most ships would fly the national flag, and most developing countries’ exports were commodities. Containerships had only just started to be deployed on East-West services.15

Today, most ships fly foreign flags and developing countries not only export raw materials. In order to participate in globalized production processes, a developing country needs to count on frequent and reliable containerized shipping services - no matter who owns the ships or which flag they fly.

Figure 3 depicts the changed participation of developing countries in seaborne trade.

Several recent empirical studies have found strong correlations between liner shipping connectivity and trade costs, in particular transport costs. A recent research project by the Economic and Social Commission for Asia and the Pacific (ESCAP) included the LSCI in an empirical study on trade costs, and concluded that "about 25% of the changes in non-tariff policy-related trade costs can be explained by the liner shipping connectivity index".16 For the estimated trade costs between a number of Asian exporters and importers, the ESCAP study found that the exporting country’s LSCI had a higher correlation with the trade costs than the importing country’s LSCI.

Individual connectivity components, such as the number of direct liner services, the vessel sizes or the level of competition on a given trade route, have also been found to be closely related to lower transport costs. Wilmsmeier et al (2006) found that increasing liner services between a pair of ports by one per cent leads to a reduction of freight charges by more than 0.1 per cent. "Given the high variability of this variable, the impact on the freight is quite high. If two ports increase their connectivity by 150 per cent (i.e. the standard deviation in our sample), the freight between them can be expected to go down by almost 10 per cent."17

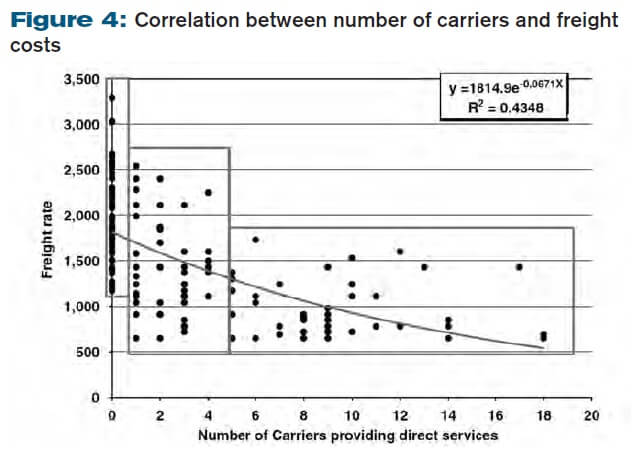

In a study on the Caribbean, Wilmsmeier and Hoffmann (2008) concluded that "The number of liner shipping companies providing direct services between pairs of countries appears to have a stronger impact on the freight rate than does distance. For routes where there is no company providing direct service, that is, where all containerised maritime trade involves at least one transhipment in a third country’s port, freight rates in our sample range from 1,170 to 3,290 USD, with an average of 2,056 USD. For routes with one to four carriers providing direct services the reported freight rates range from 650 USD to 2,250 USD with an average of 1,449 USD. If five or more competing carriers provide direct services, the freight rate ranges from 650 to 1,730 USD, averaging 973 USD. Statistically, the number of carriers explains around two fifths of the variance of the freight rate"18

Comparing the LSCI and the LPI

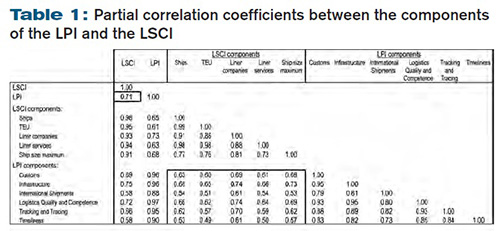

The World Bank’s Logistics Performance Index (LPI) and UNCTAD’s LSCI both aim in different ways to provide information about countries’ trade competitiveness in the area of transport and logistics. However, the scope of covered activities and countries, and the measurement approach are rather different. In spite of these differences, both indexes are statistically positively correlated with a partial correlation coefficient of +0.71 (See Table 1 and Figure 5 below).19

The LPI is a comprehensive data source on logistics performance for 155 countries in 2010, when it was generated for a second time. It takes a broadbased, multi-dimensional approach to trade logistics. The LPI covers the entire supply chain and is based on a survey of over 1,000 logistics professionals worldwide. It is a valuable tool for policymakers, researchers, and civil society, and can be used to compare performance across countries and identify key challenges within countries. The international part of LPI is based on logistics professionals’ assessments of the environment in selected trading partners across six core dimensions of logistics performance, of which a weighted average is then calculated. The six core dimensions on which the survey participants provide their scores are Customs, Infrastructure, International Shipments, Logistics Competence, Tracking and Tracing, and Timeliness. In the 2010 LPI, Germany received the highest overall score, followed by Singapore, Sweden, Netherlands and Luxembourg.

![]()

Above: The 2010 LPI, which is based on 2009 data, is correlated with the 2009 LSCI, which is based on July 2009 data.

The LSCI is generated for 162 coastal countries and territories, while the LPI is generated for 155 countries and economies, including land-locked countries20. The LPI covers a broad range of trade logistics issues, while the LSCI is limited to liner shipping. The LSCI is generated from five sets of existing "hard" data on shipping services, ships and companies, while the LPI is generated from a newly developed and much wider data base, albeit largely based on "perceptions"; in fact, in its initial version the LPI was meant to stand for "Logistics Perception Index". The broad range of issues and the reliance on survey data makes it also more difficult for the LPI to be reproduced consistently on an annual basis.

When interpreting the LSCI, it has to be noted that a country’s liner shipping connectivity is effectively closely related to its seaborne trade in manufactured goods. Even if ports and logistics services are perceived as bad and the country thus has a low LPI score, in one way or another, shipping companies will still come and transport the country’s imports and exports, leading to a high LSCI. At the same time, economies of scale and scope are important in shipping, and thus it can be expected that higher trade volumes will - ceteris paribus - also lead to more frequent and less costly shipping services, which in turn will also increase the country’s LPI.

Table 1 shows the partial correlation coefficients between the five components of the LSCI and the six components of the LPI. The overall correlation between the two indices is +0.71. Among the different components, the LPI infrastructure component is particularly highly correlated with the LSCI components Number of Companies and Largest Vessel Size. It comes as no surprise that a company’s decision to provide services from/to a country’s ports using its largest ships is closely related to the country’s available transport infrastructure. Thus, the components included in the LPI will also likely to lead to a higher LSCI, just as the components included in the LSCI will usually lead to an improved logistics performance, which is then captured in the survey data used to generate the LPI.

The liner shipping connectivity matrix

In order to facilitate further analysis of trade costs and flows, in addition to the country-level LSCI, UNCTAD has created a data base on pair-of-country connectivity data, including each coastal country’s main port(s), the maritime distance between them, and the liner shipping services between pairs of countries. We expect the resulting Liner Shipping Connectivity Matrix (LSCM) to be a useful tool for the analysis of international trade and its transport, including through so-called "gravity models".21

The UNCTAD LSCM aims at complementing the CEPII air distance and other geography variables, which are the most commonly used variables in today’s trade models.22 The idea is to improve trade modelling by incorporating relevant data on maritime transport connectivity. UNCTAD’s LSCM includes the following data for each pair of country:

- The maritime distance between the main container ports. In the cases of some large countries with several coast lines (e.g. USA, Canada et al) two or three ports are included in the initial calculation, and then the shortest option is computed and included in the LSCM.

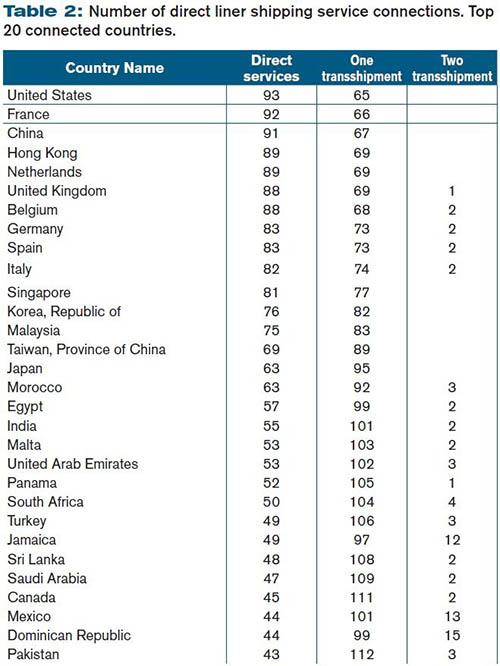

- A 1/0 variable that assumes the value 1 if there exists a direct service between the two countries, and 0 otherwise. Note that "direct" implies that there is no need for transhipment; however, the ship will usually call at other ports en route. Among 162 x 161 pairs of coastal countries covered by the LSCM, only about 19 per cent have a direct liner shipping connection.

- A new liner shipping connectivity index for each pair of countries. This index - called LSCI2 - is generated under a similar concept as the LSCI, but requires some more complex calculations in view of the fact that for 81 per cent of country pairs there are no direct liner services. Inter alia, it incorporates the number of options available to connect two countries with one transhipment. The LSCI2 is available for five years up to 2011.

Initial work with the new UNCTAD LSCM provides some interesting insights into the structure of the global liner shipping network.

In 2006, 18.4 per cent of pairs of countries were connected with each-other through a direct liner shipping services, while the remaining 81.6 per cent required at least one transhipment. In 2010, the percentage of direct connections increased by approximately half a percentage point to 18.9 per cent, leaving 81.1 per cent of country pairs requiring at least one transhipment. Out of the routes that had direct services in 2006, 83 per cent were able to keep those direct services in 2010, i.e. 17 per cent of the served routes in 2006 lost their direct service 4 years later. On the other hand, 19 per cent of the pairs of countries with direct services between them in 2010 were new connections.

Conclusion

The analysis of liner shipping connectivity provides interesting insights towards the understanding of the determinants of international trade in manufactured and other containerizable goods.

First, it allows us to observe trends in the deployment of containerships and the competitive structure of transport markets. Many smaller developing countries are confronted with the double challenge of having to accommodate larger ships while having access to fewer regular shipping services to and from a country’s ports. We observe how the industry continues to consolidate as the average number of companies per country decreases, while the average vessel size grows. Although the use of larger vessels makes it possible to achieve economies of scale and thus reduce trade costs, the extent to which cost savings are passed on to importers and exporters depends on the level of competition among carriers. Second, the country-level LSCI and the pair-of-country-level data in the LSCM allow us to undertake research into possible determinants of international tradeflows. The demand, supply and price of shipping services are mutually dependent on each other. The "demand", i.e. the volume of international trade directly depends on trade costs (freight rates) and access to liner shipping services (i.e. the "connectivity"). Freight costs depend on demand (economies of scale) and connectivity (e.g. the level of competition, vessel sizes et al). And connectivity certainly depends on demand (ships can be deployed where they are needed), but also on infrastructure, geographical location and efficient trade supporting services, such as Customs procedures or port governance.

As can be seen by comparing the LSCM data over recent years, the structure of the global liner shipping network is quite stable, but it is not cast in stone. Understanding the dynamics of countries’ connectivity within the global liner shipping networks remains a fascinating challenge for researchers and policy makers alike.

4

The percentage is calculated considering the mode

of transport by which the goods arrive at a country’s

border. See UNCTAD Transport Newsletter #38, March

2008, http://www.unctad.org/en/

docs/sdtetlbmisc20081_en.pdf.

5 In terms of ton-miles,

the share of sea- and air-borne trade is usually

even higher, as trucks and railways are used for

relatively shorter distances. See also Wally Mandryk:

Measuring Global Seaborne Trade, presented to the

annual meeting of the In International Maritime

Statistics Forum (IMSF), New Orleans, 4-6 May 2009.

http://www.imsf.info/papers/NewOrleans2009/documents/Wally_Mandryk_

LMIU_IMSF09.pdf; and David Hummels and Georg

Schaur: Time as a Trade Barrier, NBER Working Paper

17758, January 2012, http://www.nber.org/papers/w17758.pdf.

6 See UNCTAD STAT on-line:

http://unctadstat.unctad.org/wds/TableViewer/tableView.aspx?ReportId=92.

7 http://www.ci-online.co.uk

Since 2012, the data is provided by Lloyds List

Intelligence, who took over ci-online.

8 World Bank, Logistics

Performance Index..

9 World Bank, Doing Business.

http://www.doingbusiness.org.

10 The exact calculation

of the LSCI is as follows: For each of the five

components, a country’s value is divided by the

maximum value of that component in 2004, and for

each country, the average of the five components

is calculated. This average is then divided by the

maximum average for 2004 and multiplied by 100.

In this way, the index generates the value 100 for

the country with the highest average index of the

five components in 2004. UNCTAD, Review of Maritime

Transport 2011, Geneva, page 106. http://www.unctad.org/en/docs/rmt2011_en.pdf.

11 World Bank, Data. http://data.worldbank.org/indicator/IS.SHP.GCNW.XQ.

12 Tradingeconomics, http://www.tradingeconomics.com/world-bank-by-indicator-list-by-country?i=li

ner+shipping+connectivity+index+(maximum+value+in+2004+%3d+100),

13 WEF: The Global Enabling

Trade Report. http://www3.weforum.org/docs/WEF_GlobalEnablingTrade_

Report_2010.pdf

14 United Nations ECLAC:

"Concentration in Liner Shipping - its causes and

impacts for ports and shipping services in developing

countries", Santiago de Chile, 1998, http://www.eclac.org/publicaciones/

xml/5/5175/LC_G.2027.pdf.

15 http://www.unctad.org/rmt

16 UN ESCAP: Trade Facilitation

in Asia and the Pacific: Which Policies and Measures

affect Trade Costs the Most? Bangkok, 2011. http://www.unescap.org/tid/publication/swp111.pdf.

17 Gordon Wilmsmeier, Jan

Hoffmann and Ricardo Sanchez: The impact of port

characteristics on international maritime transport

costs; in: Kevin Cullinane and Wayne Talley (ed.)

"Port Economics", Research in Transportation Economics

Volume 16, Elsevier, 2006, ISBN 0-7623-1198-3.

18 Gordon Wilmsmeier and

Jan Hoffmann: Liner Shipping Connectivity and Port

Infrastructure as Determinants of Freight Rates

in the Caribbean, in: Maritime Economics & Logistics,

2008, 10, (130-151).

19 UNCTAD, Transport Newsletter

#46, Geneva, 2010. http://www.unctad.org/en/docs/

webdtltlb20103_en.pdf.

20 Since 2011, the LSCI

covers only 159 countries.

21 See for example an introductory

presentation by UN ESCAP underhttp://www.unescap.org/tid/

artnet/mtg/cbcam_d2s3.pdf.

22 See CEPII

SOMMAIRE

Préface

Par Antoine Rufenacht

Chapitre

éditorial

Par Yann Alix

Chapitre introductif

Corridors

de transport et évolution globale

des échanges

Par Gustaaf de Monie

PARTIE 1 - Approches méthodologiques

Chapitre

1

Définition

et périmètre des grands

corridors de transport fluvio-maritime

Par Claude Comtois

Chapitre 2

Les

indicateurs de performance logistique

pour les corridors de transport

Par Jean-François Pelletier

Capsule professionnelle 1

Les

observatoires des transports en Afrique

Sub-saharienne

Par Olivier Hartmann

Chapitre 3

Gouvernance

des corridors de transport et des gateways

Par Juliette Duszynski et Emmanuel

Préterre

Capsule professionnelle 2

Corridors

maritimes et terrestres : quelles stratégies

pour un opérateur de lignes régulières

?

Par Luc Portier et Alexandre Gallo

PARTIE 2 – Approches techniques

Chapitre 4

Corridors

de transport et construction du statut

juridique de l’entrepreneur de transport

multimodal

Par Valérie Bailly-Hascoët

et Cécile Legros

Capsule professionnelle 3

Gestion

des frontières, enjeux douaniers

et corridors de transport : retours d’expériences

douanières

Par Lionel Pascal

Capsule professionnelle 4

Frets

aériens et corridors humanitaires

: retours d’expérience suite

au tremblement de terre à Haïti

Par Alain Grall

Chapitre 5

Approches

technologiques et gestion des flux immatériels

sur les corridors de transport : exemples

brésiliens

Par Michel Donner

Capsule professionnelle 5

Dématérialisation

des flux d’information sur un corridor

multimodal de transport : retour d’expériences

de l’Axe Seine

Par Alain Savina et Laurie Francopoulo

PARTIE 3 – Approches stratégiques

et prospectives

Chapitre 6

L’évolution

des organisations productives et logistiques.

Impacts sur les corridors de transport

Par Jérôme Verny et Yann

Alix

Capsule professionnelle 6

Toward

efficient and sustainable transport chains:

the case of the port of Rotterdam

Par Peter de Langen

Chapitre

7

Corridors of the Sea : An investigation

into liner shipping connectivity

Par Jan Hoffmann

Capsule professionnelle 7

Evolution

des corridors de transport maritime de

pétrole brut

Par Frédéric Hardy

Chapitre

8

Strategies

and future development of transport corridors

Par Théo Notteboom

Capsule professionnelle 8

Maritime

Highway Corridors into the Caribbean Seas:

Perspective on the impact of the opening

of the expanded Panama canal in 2014

Par Fritz Pinnock and Ibrahim Ajagunna

Chapitre de conclusion

Les

corridors de transport : objets en faveur

d’une mobilité durable ?

Par Jérôme Verny

Postface

Par Marc Juhel