Publications > Editions EMS > Les corridors de transport > Towards efficient and sustainable transport chains: the case of the port of Rotterdam

|

Par

Peter de Langen

Par

Peter de Langen

Senior Advisor - Corporate Strategy

Port of Rotterdam Authority

Biographies

Dr.

Peter de Langen works at Port of Rotterdam

Authority, department Corporate Strategy as senior

advisor and is involved in various strategic renewal

projects. Peter de Langen also holds a part-time

position as professor Cargo Transport & Logistics,

at Eindhoven University of Technology, since 2008.

From 1997-2007, Peter worked at Erasmus University

Rotterdam (EUR). At Erasmus, he was engaged in research,

education and consultancy in the field of transport,

port and regional economics.

Dr.

Peter de Langen works at Port of Rotterdam

Authority, department Corporate Strategy as senior

advisor and is involved in various strategic renewal

projects. Peter de Langen also holds a part-time

position as professor Cargo Transport & Logistics,

at Eindhoven University of Technology, since 2008.

From 1997-2007, Peter worked at Erasmus University

Rotterdam (EUR). At Erasmus, he was engaged in research,

education and consultancy in the field of transport,

port and regional economics.

He published articles on port selection, port policy,

and international transport & logistics chains in

various scientific journals, provided guest lectures

at various universities abroad and participated

as speaker/ session chairman, in a large number

of (industry) conferences. His main scientific contributions

are: 1) application of cluster theories to (maritime)

transport, ports & logistics, with specific attention

for governance in clusters, 2) the analysis of coordination

in (multimodal) hinterland transport chains, 3)

analysis of the effects of concession policies,

entry barriers and intra-port competition in seaports

and, 4) the analysis of strategies of port authorities.

Peter de Langen is a co-director of the port studies

dissemination platform www.porteconomics.eu where

he also coorganises a yearly port executive training

course.

Introduction: Port of Rotterdam

Rotterdam

competes with other ports in the Hamburg-Le Havre

(HLH) range. Rotterdam is the market leader for

liquid, dry bulk and containers. The large market

shares of Rotterdam for dry and liquid bulk are

mainly explained by two factors.

Rotterdam

competes with other ports in the Hamburg-Le Havre

(HLH) range. Rotterdam is the market leader for

liquid, dry bulk and containers. The large market

shares of Rotterdam for dry and liquid bulk are

mainly explained by two factors.

First, because of the large draft (depth of entrance channels and port basins) and open access to the sea (no locks), Rotterdam can accommodate the largest bulk carriers and tankers. This is not the case in Hamburg and Antwerp (draft problems for the largest bulk vessels) and Ghent and Amsterdam (behind a lock that the largest bulk vessels cannot pass).

Second, transport from Rotterdam to sites of bulk users (oil refining, the petrochemical industry, steel production and energy production) is cheap compared to competing ports. Most of these industries receive bulk goods by river and/or pipeline. Pipeline infrastructure connects Rotterdam to the main oil refineries in North West Europe. Dry bulk (especially coal and iron ore) is mostly shipped by barge to inland destinations. This gives the ARA ports’ (Amsterdam, Rotterdam, Antwerp), that are well connected to the river Rhine, a competitive advantage over German and French ports.

As most large users of bulk commodities have stakes in bulk terminals in seaports, bulk flows do not often switch between ports. Competition between ports in the HLH range is fiercest in the container segment, not the least because of the attractive growth prospects of this market.

In the last 15 years, the container market has grown rapidly. Between 1995 and 2005, Rotterdam lost market share, especially to Antwerp and Hamburg. Hamburg has grown rapidly because of its good rail connections, its proximity to Eastern Europe, where traffic growth has been relatively high, and the position of Hamburg as a large transhipment port for cargo destined to Scandinavia and the Baltic. Antwerp has grown because of its competitively priced and productive terminals and the strong presence of forwarders.

Rotterdam has suffered from capacity shortages and a lack of intra-port competition. Furthermore, port dues in Rotterdam are relatively high, especially compared to Antwerp. The impact of such port dues on total supply chain costs may be moderate, but for shipping lines they are significant.

In the period 2007-2011, Rotterdam’s market share has increased, partly because of the development of additional capacity in Rotterdam, and because in a declining market in the crisis year 2009, Rotterdam has done better than its competitors.

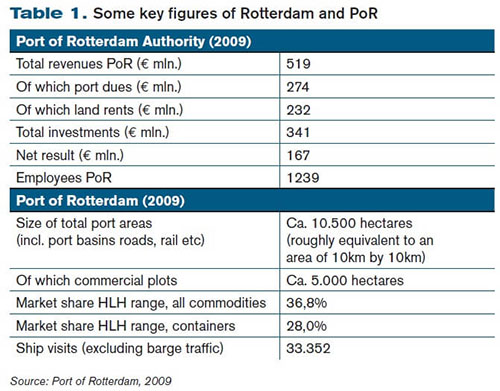

Port of Rotterdam Authority

Port of Rotterdam Authority (PoR for short) positions itself as a port developer’ with an active involvement in the port. The port authority invests substantially in public and customer specific infrastructure. Furthermore, the port authority invests substantially in other activities that have benefits for the port community, such as ICT infrastructure (through the establishment of Portbase, a subsidiary of the port authorities of Rotterdam and Amsterdam), and port marketing.

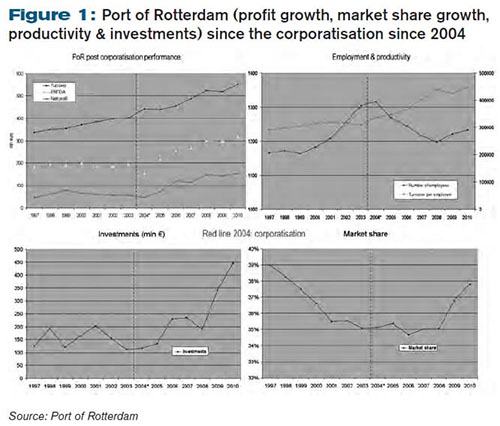

In 2004, the institutional position of PoR changed from a municipal department to a public corporation. The management (Executive Board) of PoR is no longer controlled directly by the municipality but by a Supervisory Board. Supervisory Board members have experience in managing (public) corporations, especially in the transport and energy industries. The shareholders (the municipality of Rotterdam and the national government) have a formal influence at the annual shareholders meeting. This governance structure is rather exceptional in the port industry; in most other publicly owned ports the political influence is larger. Figure 1 shows the performance of PoR, in terms of profit growth, market share growth, productivity and investments. The corporatisation in 2004 has clearly had a positive effect on the performance of PoR. The increased performance enables continued high investment levels of PoR in the port complex.

The core activity of PoR is to develop the port area and lease sites in port of Rotterdam to companies, often multinationals, such as Shell, Exxon, Vopak, BASF, Hutchinson Port Holdings (HPH) and APMT. From 2001-2007 (last year for which data are available), private companies in the port have invested roughly 1.5 billion per year in the port area, compared to investments of PoR of around 150-200 mln. per year around 10% of the private investments. Thus, attracting private investments (terminal equipment, new plants, expansion of terminals and storage facilities, and so on) is crucial for the long term competitiveness of the port.

Vision for port of Rotterdam: leading in efficiency and sustainability

The track record of port of Rotterdam is strong. The port is by far Europe’s largest port, and the largest bulk port in the world. In the World Economic Forum (WEF) competitiveness report, the Netherlands ranks consistently in the top three worldwide on quality of port infrastructure (WEF, 2012). The Netherlands also ranks high in the Worldbank Logistics Performance Index. PoR aims to maintain a leadership role in the global port industry, and focuses, both in the corporate business plan and in the port vision, on leadership in efficiency and sustainability.

Reasons of focusing on efficiency

As Rotterdam is not the cheapest port, both for port dues and for land rents, and as the wage level in the Netherlands is relatively high (keeping in mind that labour costs are up to 50% of total operational costs of container terminals and similarly high for trucking), Rotterdam needs to continue to develop a competitive edge through efficiency. There are different potential sources of superior efficiency, including:

- Scale economies in terminal operations and inland transport.

- Better coordination of intra-port freight flows.

- More seamless supply chains (e.g. information flows as well as financial flows).

- Better hinterland connectivity, resulting in lower generalised costs for port users.

- Higher productivity of freight transport companies.

A competitive edge through superior efficiency continuously needs to be re-enforced, as rivals also invest to improve efficiency and successful projects become available for the port industry at large. But a culture of continuous improvement in Rotterdam can provide at a deeper level a lasting driver of leadership in efficiency. This leads us to stress the importance of institutions, such as a culture of trust, cooperation, innovation, as well as cooperation enhancing institutions (as an interesting note, Harris argues that the Dutch East India company that was active in the 16th century, can be thought of as an cooperation enhancing institution). While corporate governance is often multinational, cluster governance remains highly localised and consequently explain why ports in different regions follow widely diverging development paths. Rotterdam’s past path is based on leadership through efficiency, and the key challenge is to remain on this path of the port.

-

Reasons of focusing on sustainability

Transport systems have significant impacts on climate change, accounting for between 20 and 25 per cent of world energy consumption and CO2-emissions. Greenhouse gas emissions from transport are increasing at a faster rate than any other sector. Given the widely expected future growth of transport, both for passengers and for freight, there is an urgent need for a transition away from fossil fuels and towards more sustainable transport, both to combat global warming and because of increased scarcity and rising price- of oil. For freight this issue is particularly relevant in the container sector, where fuel consumption is highest (due to the relatively high speed of container vessels) and the share of road transport for the hinterland leg is relatively high. In comparison, many liquid bulk flows are transported by pipeline, a much more sustainable hinterland mode, while bulk flows are transported inland by train or barge, also more environmentally friendly than road transport. The drive towards more sustainable supply chains is led by shippers. Various large shippers (including Unilever, -25% in 2012 and Sony, -30% in 2015, for emission targets of more companies see http://www.ecodesk. com) have announced ambitious sustainability goals2.

It is important to note that efficiency and sustainability are virtually always complementary: more efficiency leads to reduced empty trucks, more intermodal transport, better route planning and so on. All of these also improve sustainability. Efficiency and sustainability gains are possible in all industries, and likewise in all parts of freight transport. However, for freight transport, the potential for efficiency gains in inland transport is especially huge. This is because of the interorganisational complexity of hinterland transport (see Van der Horst aand De Langen, 2008) is huge. For this reason, we focus on this part of the freight transport chain in the remainder of this paper.

-

Activities of Port of Rotterdam Authority

It is impossible to describe in detail all activities of PoR aimed at improving the sustainability and efficiency of inland transport.

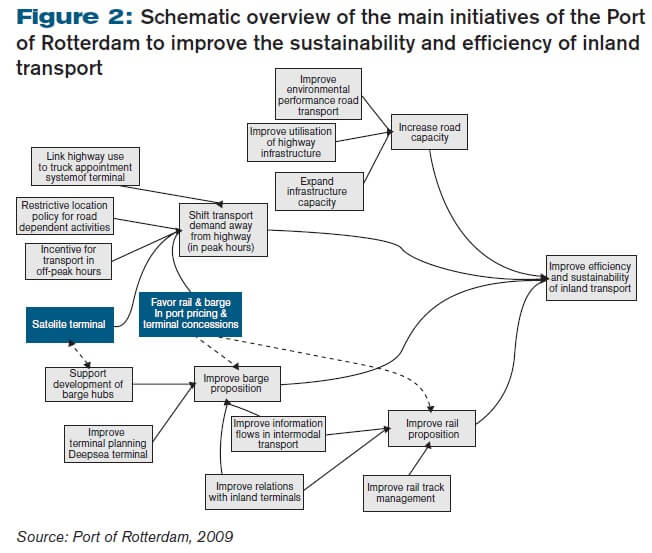

In the remainder of this paper we focus on the concession awarding process for a container terminal on MV2 and the satellite terminal project developed by PoR (the highlighted projects in figure 1). Both projects are unique worldwide.

Concession awarding processes and modal split requirements

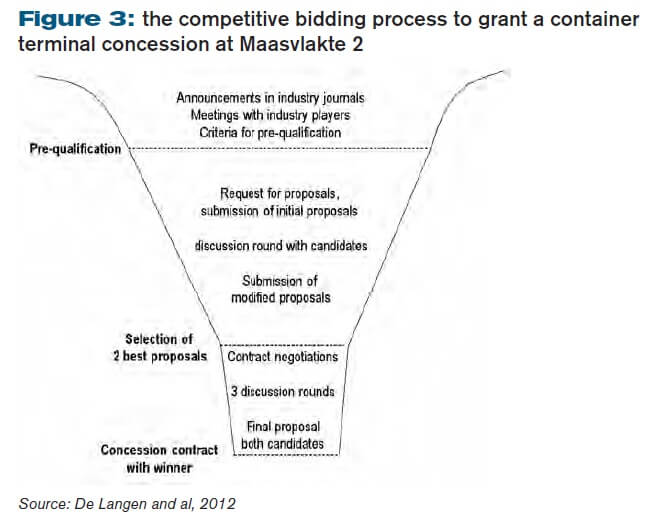

PoR invests substantially in port expansion, through the Maasvlakte 2 (MV2) project. MV2 consists of roughly 1000 acres of port land (and roughly 1000 acres of water basins). The total construction costs are estimated to be 2.9 billion. PoR bears the costs and risks of building Maasvlakte 2, and receives the revenues from concession contracts and port dues. The project was developed with a business case approach: the revenues (port dues, land rents) are sufficient to cover investment and operational costs and generate sufficient returns. This port development approach prevents the publicly-funded development of port sites that later prove of limited value3. The project is financed entirely by PoR, partly with equity and partly with loans from banks (in total around 2 billion). One important plot of Maasvlakte 2, was concessioned to a terminal operator, using competitive bidding (see De Langen et al, 2012). In this process, PoR provides invites bids and develops a method to rank bids. Figure 2 shows the competitive bidding process.

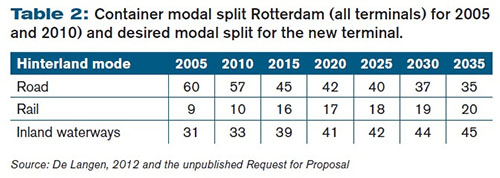

In line with the commitment to sustainability for the port as a whole, and keeping in mind the need to secure stakeholder support for the construction of MV2, PoR decided to make sustainability an important item in the assessment of bids. The most relevant goal regarding sustainability is to increase the share of intermodal transport. Both rail and barge are more sustainable than road transport. Thus PoR developed a desired modal split, that candidates for the concession need to match (see table 1).

This table shows the huge ambition to shift the modal split towards more intermodal transport. This improves the sustainability of the port, gives terminal operators the incentives to develop strategies to improve the modal split, and sends a clear message to all stakeholders that policies and investments are required to realise this shift.

A satellite terminal (transferium)

The largest part of the containers handled in Rotterdam, around 6.7 mln TEU are direct deepsea flows’. Some of these containers are opened in distribution centers in the port area, but the vast majority is destined to the hinterland, both in the Netherlands and in countries such as Germany, Austria and Belgium.

Given the past growth, expected future growth, congestion of roads and increased pressure on the transport sector to move traffic from the road to other, more sustainable, transport modes, hinterland accessibility is one of the main challenges for Rotterdam’s port. While there is substantial additional capacity in the inland shipping system, and also additional capacity for rail transport, after completion of the Betuwe Line, a dedicated railroad that connects Rotterdam to the German rail system, the highway infrastructure is congested, and capacity expansion is problematic given lack of space and limited societal support for new highway infrastructure, especially in the densely populated Rotterdam region.

So far, Rotterdam is the only port where the port authority has taken the initiative to develop a container transferium at least to our knowledge. Central to the transferium concept is the idea that trucks deliver their container not in the port itself, but at a transferium, located outside the congested port area. The key for a successful transferium is the price advantage: using it must be cheaper than transport on the same route by truck. Next to this advantage, a transferium can potentially also create value for deepsea terminals as a transferium can help reduce dwell times and reduce the peak in the arrival pattern of trucks at the gate of the terminal. Furthermore, for shippers, a transferium can increase the reliability of transport to/from the port, as the congested port and port access highways are avoided. Given the need to be competitive with direct trucking, sufficient scale is important, as both terminal operations and inland shipping are characterised by important scale economies.

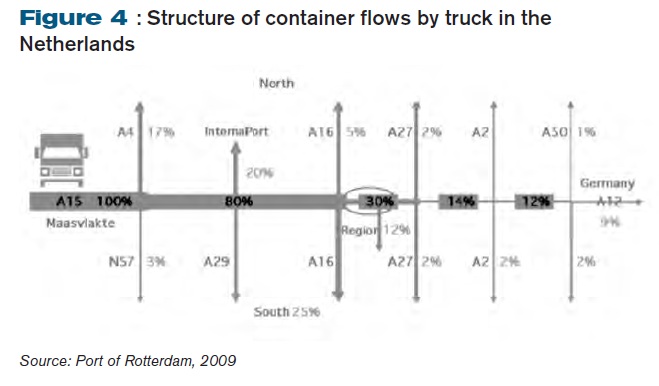

This figure shows that the truck flows rapidly dissipate. Thus, a transferium needs to be placed close to the port. Only in this case is the market sufficiently large. In the case of Rotterdam, a location was selected in the circled part of the A15, where roughly 30% of all container trucks to/from the port pass by. In the Rotterdam case, the total market was initially estimate to be around 500.000- 750.000 TEU, but with substantial growth expectations, of around 2-3% growth of truck moves per year. This market is sufficiently large for a facility that once fully developed, can handle around 180.000 TEU, so needs to capture around 15- 25% of the truck traffic that passes by. A facility with such a volume can fill twice daily barge services to the deepsea terminals.

In terms of costs, a business case was developed, where revenues for the operator of roughly 70 per container (handling and transport) were assumed. For trucking companies, this is a competitive price, as trucking the additional 60km to the deepsea terminals, through the congested port area and with waiting times at the terminal gate, and the return journey can easily take four hours. Only gasoline and truck driver expenses are already higher than the 70 per container. In the business case, investments for the operator are limited, as Port of Rotterdam takes on the investments in the terminal site, and leases this site, for a competitive price, to an operator.

Port of Rotterdam Authority (PoR) has taken the initiative, developed the concept, and played a leading role in obtaining support and approval from the authorities, both national and local. PoR commercialised the business opportunity, in this case through competitive bidding, but with a keen eye for the stakeholder support for the operator.

Conclusions

Ports play important roles in regional, national and international economic development, by providing connectivity. They connect consumers and producers with world markets. Over the past decades, this connectivity has improved significantly. New improvements will further increase connectivity, and create value for port users.

Such new improvements will not emerge spontaneously, but require innovations, cooperation, experiments, new technologies and so on. Ports with relative much of these activities will do better than ports where only existing best practices are introduced. Rotterdam is such a hotspot of innovative activity, due to its scale, culture of cooperation, forward looking policies, quality of the companies in the port and quality of research and development in transport and logistics. The key challenge is to remain such a hotspot. The two projects discussed above are examples of innovative projects, aimed at further improving the efficiency and sustainability of the port. They may not be feasible or sensible in other ports, but do provide a best practice that may be relevant for the port industry at large.

Références bibliographiques

HAEZENDONCK, E., PISON, G., ROUSSEEUW, P., STRUYF, A. and VERBEKE, A. (2001) « The core competences of the Antwerp seaport: an analysis of ‘‘port specific” advantages”, International Journal of Transport Economics, 28(3), 325-349.

HARRIS, R., (2005) ‘‘The Formation of the East India Company as a Cooperation- Enhancing Institution”, (December 2005). Available at SSRN: http://ssrn.com/abstract= 874406 or doi:10.2139/ssrn.874406

VAN DER HORST, M. R. and LANGEN DE, P.W. (2008) ‘‘Coordination in Hinterland Transport Chains: A Major Challenge for the Seaport Community”, Maritime Economics and Logistics 10, pp. 108-129.

LANGEN, P.W. DE and PALLIS, A.A. (2006) ‘‘Analysis of the Benefits of Intra-port Competition”. International Journal of Transport Economics 33(1), 69-86.

LANGEN, P.W. DE, VAN DEN BERG, R. and WILLEUMIER, A. (2012) ‘‘A new approach to granting terminal concessions; the case of the Rotterdam World Gateway terminal”, Maritime Policy and Management, 39 (1).

2

The precise calculation of the carbon footprint

for a specific shipment is still difficult. While

some shipping companies provide carbon calculators,

these are not based on specific information about

a specific shipment. Furthermore, such calculators

are mostly limited to port-to-port transport and

do not include all emissions in the door-to-door

chain

3 MV2 is being built in

2 phases. The demand for land on Maasvlakte 2 determines

whether and when the second phase will be constructed.

SOMMAIRE

Préface

Par Antoine Rufenacht

Chapitre

éditorial

Par Yann Alix

Chapitre introductif

Corridors

de transport et évolution globale

des échanges

Par Gustaaf de Monie

PARTIE 1 - Approches méthodologiques

Chapitre

1

Définition

et périmètre des grands

corridors de transport fluvio-maritime

Par Claude Comtois

Chapitre 2

Les

indicateurs de performance logistique

pour les corridors de transport

Par Jean-François Pelletier

Capsule professionnelle 1

Les

observatoires des transports en Afrique

Sub-saharienne

Par Olivier Hartmann

Chapitre 3

Gouvernance

des corridors de transport et des gateways

Par Juliette Duszynski et Emmanuel

Préterre

Capsule professionnelle 2

Corridors

maritimes et terrestres : quelles stratégies

pour un opérateur de lignes régulières

?

Par Luc Portier et Alexandre Gallo

PARTIE 2 – Approches techniques

Chapitre 4

Corridors

de transport et construction du statut

juridique de l’entrepreneur de transport

multimodal

Par Valérie Bailly-Hascoët

et Cécile Legros

Capsule professionnelle 3

Gestion

des frontières, enjeux douaniers

et corridors de transport : retours d’expériences

douanières

Par Lionel Pascal

Capsule professionnelle 4

Frets

aériens et corridors humanitaires

: retours d’expérience suite

au tremblement de terre à Haïti

Par Alain Grall

Chapitre 5

Approches

technologiques et gestion des flux immatériels

sur les corridors de transport : exemples

brésiliens

Par Michel Donner

Capsule professionnelle 5

Dématérialisation

des flux d’information sur un corridor

multimodal de transport : retour d’expériences

de l’Axe Seine

Par Alain Savina et Laurie Francopoulo

PARTIE 3 – Approches stratégiques

et prospectives

Chapitre 6

L’évolution

des organisations productives et logistiques.

Impacts sur les corridors de transport

Par Jérôme Verny et Yann

Alix

Capsule professionnelle 6

Toward efficient and sustainable

transport chains: the case of the port

of Rotterdam

Par Peter de Langen

Chapitre

7

Corridors

of the Sea : An investigation into liner

shipping connectivity

Par Jan Hoffmann

Capsule professionnelle 7

Evolution

des corridors de transport maritime de

pétrole brut

Par Frédéric Hardy

Chapitre

8

Strategies

and future development of transport corridors

Par Théo Notteboom

Capsule professionnelle 8

Maritime

Highway Corridors into the Caribbean Seas:

Perspective on the impact of the opening

of the expanded Panama canal in 2014

Par Fritz Pinnock and Ibrahim Ajagunna

Chapitre de conclusion

Les

corridors de transport : objets en faveur

d’une mobilité durable ?

Par Jérôme Verny

Postface

Par Marc Juhel