Publications > Capgemini Consulting > Third-Party Logistics Study > Current State of the 3PL Market

|

![]()

Current State of the

3PL Market

Shippers Reflect Continued Confidence

with Use of 3PL Services

Results of the 2012 16th Annual Third-Party Logistics Study once again reaffirmed that third-party logistics providers continue to provide strategic and operational value to many shippers across the globe. Shippers consider logistics and supply chain management as key contributors to their overall business success, and approximately three-quarters of survey respondents say 3PLs provide new and innovative ways to improve logistics effectiveness.

These

results are based on survey responses from 1,561

industry executives and managers representing users

and non-users of 3PL services (referred to as shippers

or shipper respondents throughout this report),

as well as 697 executives and managers representing

firms that provide 3PL services (called 3PLs or

3PL respondents). 3PLs were added to the survey

group in 2009 in order to capture both sides of

the buyer-seller relationship.

The number of usable survey responses continues

to rise each year, with a significant increase for

the 2012 Study.

Please see About the Study for detailed information about survey responses and the four streams of research used to fully analyze the state of the 3PL market: a web-based survey, desk research, focus interviews, and facilitated workshop sessions at Capgemini Accelerated Solutions Environment® (ASE) locations in Chicago, Illinois, and Utrecht, The Netherlands, and at the 2011 eyefortransport 3PL Summit in Atlanta, Georgia.

Current Global Economic Climate and Use of 3PLs

As acknowledged in

our Annual 3PL Studies over the past two to three

years, economic volatility and uncertainty have

impacted global business markets and in turn, global

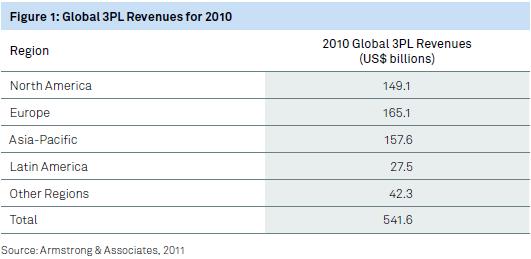

markets for 3PL services. Figure 1 includes data

from Armstrong & Associates that estimates the

magnitude of global 3PL revenues for 2010 (US $541.6B),

and provides breakdowns for the four major geographies

that are included in the 2012 3PL Study.

Global 3PL revenues reported for 2010 represent

an increase of 6.8% over those reported in 2009,

confirming the general trend toward improving global

business conditions. Focusing specifically on the

US, 3PL revenues reported by Armstrong &

Associates have increased from US $107.1B in 2009

to US $127.3B in 2010, and are expected to increase

to US $141.2B in 2011.

Generally, these reflect the somewhat-improving

global business environment and ongoing economic

globalization.

The Competitive Starting Line Has Been Re-Set

The chief reason for conducting the 2012 3PL Study is to update our knowledge of 3PL-shipper relationships, and to learn how both types of organizations are using these relationships to improve and enhance their businesses and supply chains. Many shippers are currently in search of new and innovative global supply chain strategies, suggesting new opportunities for 3PLs to make significant contributions to supply chain efficiency and effectiveness. Many shippers and 3PLs agree that today’s business challenges represent some version of a ‘‘new normal,” driving the need for both types of organizations to identify and implement new strategies for success. In effect, the starting line has been re-set, injecting a new, highly invigorated and highly competitive spirit into the logistics business environment.

‘‘Today’s 3PL marketplace is experiencing significant change. Established 3PLs are recalibrating their business models to provide greater value to their shipper-customers,” noted one prominent 3PL industry observer. ‘‘At the same time, they are looking over their shoulders at emerging sources of competition and the new and innovative offerings they are bringing to market.”

Spending on Logistics and 3PL Services

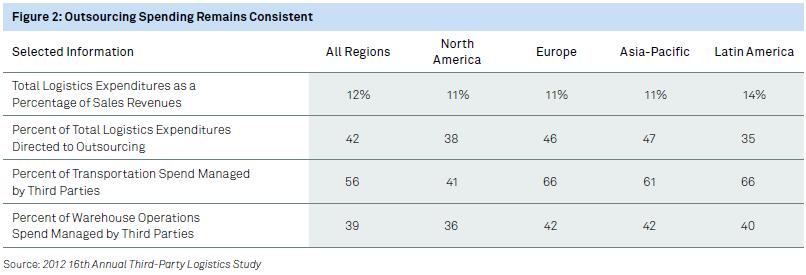

As seen in Figure 2, shipper respondents to the 2012 3PL Study report that total logistics expenditures represent an average of 12% of their companies’ sales revenues. Total logistics expenditures include transportation, distribution, warehousing and value-added services. Regional differences range from 11% in each of three regions to Latin America’s 14% of company sales revenues.

Shippers devote an average 42% of this total to outsourcing, the same as reported in last year’s study. That suggests that in comparison with the previous year, average changes in expenditures for outsourced logistics have been proportional to changes in total logistics expenditures. The average percentages of logistics spending shippers devote to outsourcing by region are also similar to last year. A new series of questions in the 2012 3PL Study asked shippers to report the percentages of transportation and warehousing spend that are managed by third parties. As indicated in Figure 2, the overall average for transportation was 56%, but the regional averages ranged from 41% in North America, to more than 60% for shippers in Europe, Asia-Pacific and Latin America. The average warehouse operations spend managed by third parties was 39%, with only modest variation by individual region.

Reported Changes in Use of 3PL Services

In recent years’

studies, we began to ask shippers whether they

were increasing their use of outsourced logistics

services, or returning to insourcing many of them.

The responses represent an interesting record

of the shifting use of 3PL services:

- Increasing

use of 3PL services: Nearly two-thirds

(64%) of shipper respondents report an increase

in their use of outsourced logistics services,

and 76% of 3PL respondents agree this is what

they are seeing from their customers. Regionally,

58% of North America shippers reported increased

use, as well as 57% of European, 78% of Asia-Pacific

and 73% of Latin American shippers.

- Returning

to insourcing: Consistent with the churn

that occurs each year with some companies increasing

outsourcing and others bringing logistics activities

back in-house, an average of 24% of shipper respondents

are returning to insourcing some of their logistics

activities, and 37% of 3PL respondents observe

that some of their customers are returning to

insourcing logistics activities.

- Reducing or consolidating the number of 3PLs used: Slightly over one-half (58%) of shipper respondents are consolidating the number of 3PLs they use, and 72% of 3PLs feel that customers in general are reducing or consolidating the number of 3PLs they use. This general trend toward consolidation is consistent with contemporary trends in procurement and strategic sourcing.

Interestingly, the percentage of shippers increasing/decreasing their use of 3PL services is very close to the figures we reported in last year’s study. So, again this year, there is strong evidence that the predominant direction among shippers is to move toward increased use of outsourced logistics services.

3PL-Shipper Relationships Continue to Progress and Improve

Similar to last year’s study, 88% of shippers view their 3PL relationships as generally successful, compared with 94% of 3PL respondents. Shippers’ ratings are consistent across regions: North America 89%; Europe 88%; Asia-Pacific 89%; and Latin America 87%.

Somewhat fewer shippers, 71%, indicate that 3PLs provide them with new and innovative ways to improve logistics effectiveness; 91% of 3PL providers feel that this statement accurately characterizes the services they provide. The gap continues between the ratings that shipper respondents assign to various aspects of the 3PL-shipper relationship and the more positive evaluations provided by the 3PL respondents themselves.

Success Factors: According to the survey findings, the following are key ingredients to successful 3PL-shipper relationships:

- Openness,

transparency and good communication:

While 69% of shipper respondents are satisfied

with the openness, transparency, and communication

received from 3PLs, only 62% of 3PLs are satisfied

with these characteristics in their relationships

with customers. So, apparently there is a need

for both parties to consider the value that could

be gained by being more willing to share appropriate

information with their business partners.

- Agility

and flexibility to accommodate current and future

business needs and challenges: Nearly

all (98%) 3PLs feel that their customers expect

them to be sufficiently agile and flexible to

accommodate their (shippers’) current and

future business needs and challenges.

But just 68% of shippers judge their 3PLs as sufficiently agile and flexible, down from 72% last year. This aspect of 3PL-customer relationships clearly needs improvement, and deserves careful watching.

- Interest

in ‘‘gainsharing” between 3PLs and

shippers: Gainsharing comes up frequently

during our shipper workshops, and we are receiving

mixed signals regarding this form of shipper-3PL

collaboration. This year 56% of 3PL respondents

and 42% of shippers (versus 56% last year), report

engaging in gainsharing arrangements. While many

shippers consider gainsharing to be a useful incentive

for themselves and their 3PL providers to work

toward agreed-upon objectives and in keeping with

the principles of good collaboration, others seem

to feel that the basic agreement with a 3PL should

cover all areas where performance is expected,

and that it is not necessary or appropriate to

engage in gainsharing practices. Interest in gainsharing

may be diminishing somewhat due to slight improvements

in the global business economy. We plan to follow

this closely in future studies.

- Interest

in collaborating with other companies, even competitors,

to achieve logistics cost and service improvements:

When this question was asked last year for the

first time, 68% of shipper respondents and 80%

of 3PLs expressed interest in these strategies.

This year these percentages dropped to 44% and 67%, respectively. So, while last year we stated it was ‘‘reassuring to see percentages that suggest a true interest by both parties in working with other companies, even competitors,” perhaps the easing of global economic conditions have made this less of a priority.

We will continue to focus on this issue in future studies.

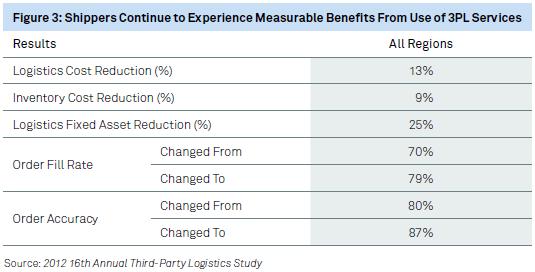

Measurable Benefits: Shipper respondents experience measurable benefits from 3PL services, as seen in Figure 3. Metrics relating to logistics cost reduction, inventory cost reduction, and logistics fixed asset reduction are consistent with what was reported in the two previous years’ studies.

Shippers also report improvements in order fill rate and order accuracy resulting from use of 3PLs, although the absolute levels of these metrics are a little lower than those reported in both the 2009 and 2010 3PL Studies. This may be an indicator of the continuing impact of the global economic recession.

Finally, survey results showed that 60% of the shipper respondents report their use of 3PLs has led to ‘‘year-over-year incremental benefits;” and 88% of 3PL respondents agree. Despite the positive success ratings perceived by both shippers and 3PLs, there appears to be opportunity to enhance the benefits experienced by users of outsourced logistics services.

Information Technology

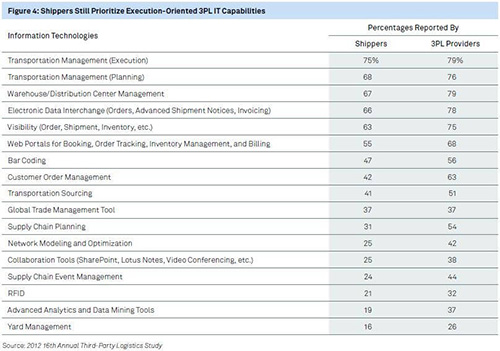

Figure 4 summarizes the information technology (IT) capabilities that shippers and 3PLs feel are ‘‘must haves” for 3PLs to successfully serve customers. Overall, the most needed capabilities are those that relate directly to execution-oriented activities and processes such as transportation, warehouse/ DC management, electronic data interchange, visibility, etc. Others that have somewhat lower rankings tend to be more strategic and analytical.

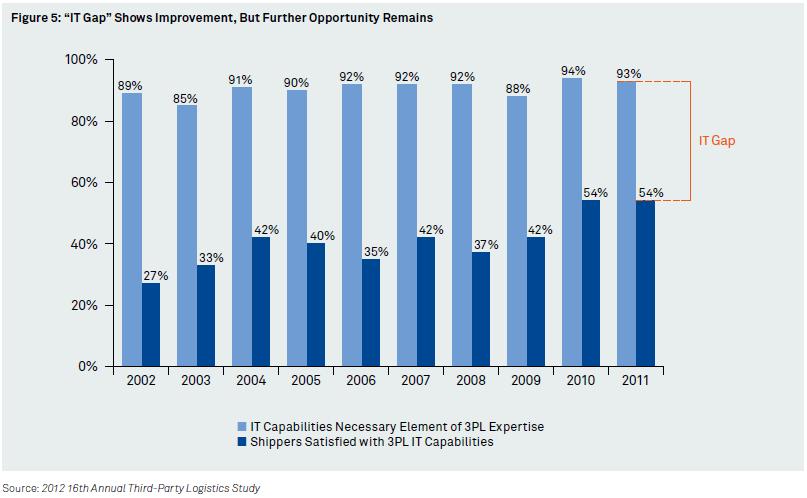

Highlighted in Figure 5 is a ten-year view of shippers’ opinions on whether they feel information technologies are a necessary element of 3PL expertise, and whether they are satisfied with their 3PL providers’ IT capabilities, the difference that has become known as the ‘‘IT Gap.” In recent years there has been a modest increase in the percentages of shippers who indicate satisfaction with the IT capabilities of their 3PLs; in fact, it is worth noting that the satisfaction rate has doubled since this question was first asked in 2002. Despite this improvement, the opportunity remains to further narrow the gap between these two ratings. Similar to last year’s study, 68% of 3PLs feel that their customers are satisfied with the IT services they provide.

What 3PL Users Outsource and What 3PL Providers Offer

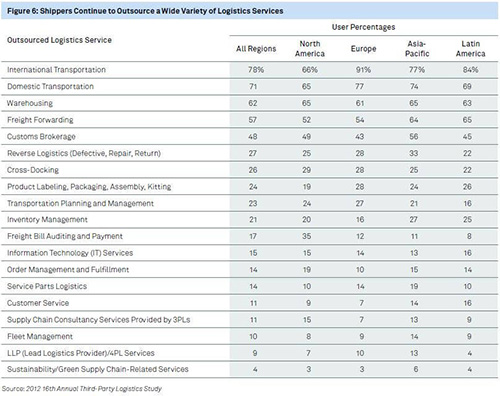

Figure 6 shows the percentages of shipper respondents that outsource specific logistics activities. Provided below are some general observations about this year’s results and the contrasts they reveal from previous years:

- Transactional,

operational, and repetitive activities tend to

be the most frequently outsourced. These include

international and domestic transportation (78%

and 71% across all regions studied), warehousing

(62%), freight forwarding (57%) and customs brokerage

(48%). This usage varies across each of the regions.

Another observation is that for the most part,

the percentages indicated in Figure 6 for the

‘‘all regions” results are somewhat

lower than comparable percentages from the previous

year’s study. This may be explained somewhat

by the fact that the current study yielded a higher

percentage of shipper respondents in the lowest

revenue category than in the previous year’s

study, as noted in the About

the Study

chapter later in this report.

Further analysis of the available data confirmed that the higher the sales category, the higher the average number of logistics activities outsourced.

- Perhaps due to

the globally volatile business environment, the

percentage of shippers outsourcing international

transportation declined from 84% in 2009 to 75%

in 2010, and now has increased slightly to 78%.

Over the same time frame, the reported use of

customs brokerage declined from 71% to 58% to

48% and the reported use of freight forwarding

services declined from 65% to 53% and then increased

to 57%.

- The less-frequently reported activities indicated in Figure 6 tend to be somewhat more strategic, customer-facing, and IT-intensive. Examples include: IT services; supply chain consultancy services; order management and fulfilment; fleet management; customer service; and LLP/4PL services.

Figure 7

is a summary of the types of logistics services

provided by 3PLs participating in the 2012 survey

and reveals that many 3PLs provide a wide range

of services.

Based on findings from last year, it is very common

for 3PLs to offer many, or even most, of the range

of services included in the question: the typical

model is for 3PLs to offer a substantial number

of services to respond effectively to their customers

and their logistics needs.

Earlier, the 2008 3PL Study included a special topic focus on shippers’ expectations and usage of 3PLs as a part of their green supply chain initiatives. Follow-up questions on this topic in the 2012 3PL Study reveal that 29% of shippers rely on 3PLs to provide visibility to fuel efficiency and carbon emissions information. Fully 53% of shippers say fuel efficiency and carbon emissions have become an important part of their 3PL procurement decision processes.

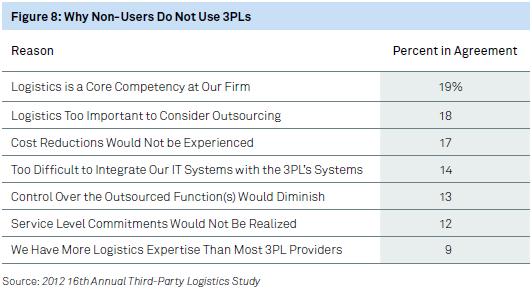

The Voices of Current Non-Users of 3PL Services

The Annual 3PL Study survey also reaches a substantial number of organizations who do not currently use 3PLs. One objective of this study is to provide insight into shippers’ decisions not to outsource. As indicated in Figure 8, the most common reasons are core competency, the importance of logistics, realization of cost reductions, integrating IT systems with 3PL systems and control over outsourced activities. While there is a certain logic behind using these concerns to support a decision not to outsource, our discussions with shippers indicate that sometimes these very issues are used by other companies to justify their decision to outsource certain logistics services.

|

Index:

- Executive Summary

- Current State of the 3PL Market

- Emerging Markets

- Electronics

- Talent Management

- Strategic Assessment

- About the Study

About Capgemini Consulting

With more than 115,000 people in 40

countries, Capgemini is one of the world’s

foremost providers of consulting, technology

and outsourcing services. The Group reported

2010 global revenues of EUR 8.7 billion.

Together with its clients, Capgemini creates

and delivers business and technology solutions

that fit their needs and drive the results

they want. A deeply multicultural organization,

Capgemini has developed its own way of

working, the Collaborative Business ExperienceTM,

and draws on Rightshore®, its worldwide

delivery model.

Capgemini Consulting is the Global Strategy

and Transformation Consulting brand of

the Capgemini Group, specializing in advising

and supporting organizations in transforming

their business, from the development of

innovative strategy through to execution,

with a consistent focus on sustainable

results. Capgemini Consulting proposes

to leading companies and governments a

fresh approach which uses innovative methods,

technology and the talents of over 3,600

consultants worldwide.